All Categories

Featured

Table of Contents

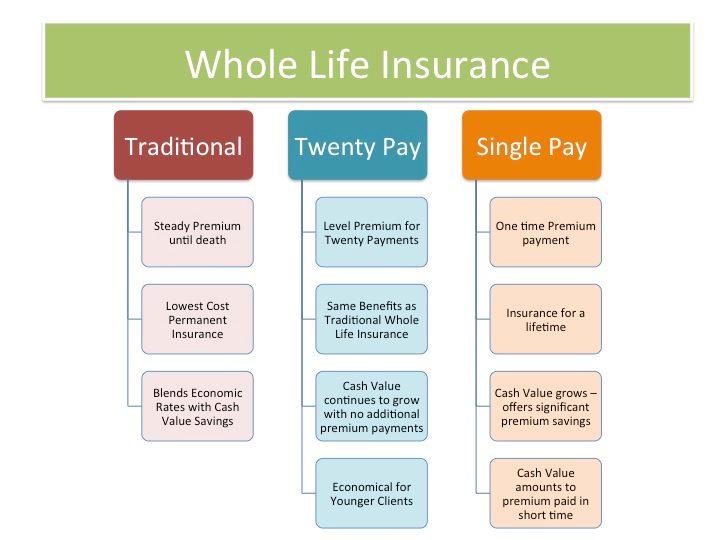

The are whole life insurance policy and universal life insurance. expands cash value at a guaranteed rate of interest and additionally via non-guaranteed dividends. grows cash worth at a taken care of or variable price, depending upon the insurer and plan terms. The money worth is not contributed to the survivor benefit. Money value is a function you capitalize on while active.

After one decade, the money value has grown to approximately $150,000. He secures a tax-free loan of $50,000 to begin an organization with his bro. The policy funding passion rate is 6%. He pays back the lending over the next 5 years. Going this course, the rate of interest he pays returns into his policy's cash worth rather than a financial establishment.

Public Bank Visa Infinite

Nash was a financing specialist and follower of the Austrian college of business economics, which promotes that the value of products aren't clearly the result of traditional financial frameworks like supply and need. Rather, individuals value money and products differently based on their economic condition and demands.

Among the challenges of traditional banking, according to Nash, was high-interest prices on fundings. Also many individuals, himself included, entered monetary difficulty due to dependence on financial establishments. Long as banks set the passion prices and car loan terms, individuals really did not have control over their own wealth. Becoming your own lender, Nash determined, would certainly put you in control over your economic future.

Infinite Financial needs you to own your financial future. For ambitious individuals, it can be the finest monetary device ever. Below are the advantages of Infinite Banking: Perhaps the single most advantageous facet of Infinite Banking is that it improves your money circulation.

Dividend-paying whole life insurance policy is extremely reduced risk and supplies you, the insurance holder, a great bargain of control. The control that Infinite Financial supplies can best be grouped into two classifications: tax obligation advantages and possession defenses - how infinite banking works. Among the factors whole life insurance policy is suitable for Infinite Financial is how it's tired.

Rbc Royal Bank Visa Infinite Avion

When you use whole life insurance policy for Infinite Banking, you get in right into an exclusive contract in between you and your insurance coverage company. These protections might vary from state to state, they can consist of protection from possession searches and seizures, protection from judgements and security from financial institutions.

Whole life insurance policy plans are non-correlated assets. This is why they work so well as the monetary structure of Infinite Financial. Regardless of what takes place in the market (supply, realty, or otherwise), your insurance plan retains its worth. Too several people are missing out on this vital volatility barrier that helps secure and grow riches, instead breaking their money into two pails: financial institution accounts and investments.

Market-based financial investments expand wealth much quicker however are exposed to market variations, making them naturally risky. Suppose there were a third pail that provided safety yet also moderate, surefire returns? Whole life insurance policy is that third container. Not only is the rate of return on your whole life insurance policy plan guaranteed, your survivor benefit and premiums are additionally assured.

This structure aligns perfectly with the principles of the Continuous Riches Method. Infinite Financial attract those looking for better economic control. Below are its primary advantages: Liquidity and accessibility: Plan fundings provide prompt access to funds without the restrictions of conventional financial institution loans. Tax obligation efficiency: The cash money value grows tax-deferred, and policy fundings are tax-free, making it a tax-efficient device for building wealth.

Bank On Yourself Insurance Companies

Possession defense: In several states, the cash money value of life insurance policy is shielded from lenders, adding an added layer of financial safety. While Infinite Banking has its qualities, it isn't a one-size-fits-all remedy, and it includes significant disadvantages. Right here's why it might not be the very best strategy: Infinite Financial often requires detailed policy structuring, which can perplex insurance policy holders.

Envision never having to fret about bank loans or high interest prices once more. That's the power of infinite banking life insurance policy.

There's no set funding term, and you have the freedom to choose the payment schedule, which can be as leisurely as paying back the car loan at the time of fatality. This adaptability expands to the maintenance of the fundings, where you can choose interest-only settlements, maintaining the funding equilibrium flat and convenient.

Holding cash in an IUL dealt with account being credited interest can often be much better than holding the cash money on down payment at a bank.: You've always desired for opening your very own bakeshop. You can borrow from your IUL plan to cover the preliminary costs of renting a room, buying equipment, and hiring personnel.

Banking Life

Individual financings can be acquired from standard banks and debt unions. Obtaining money on a credit card is usually extremely costly with yearly percentage prices of interest (APR) typically getting to 20% to 30% or even more a year.

The tax obligation therapy of policy fundings can differ considerably relying on your country of residence and the details regards to your IUL policy. In some areas, such as North America, the United Arab Emirates, and Saudi Arabia, plan car loans are generally tax-free, supplying a significant benefit. In various other territories, there may be tax implications to think about, such as prospective tax obligations on the financing.

Term life insurance policy only supplies a fatality advantage, without any type of cash money worth buildup. This implies there's no cash money value to obtain versus. This article is authored by Carlton Crabbe, President of Resources forever, a specialist in giving indexed universal life insurance policy accounts. The information supplied in this post is for instructional and informative objectives only and need to not be interpreted as financial or investment recommendations.

For loan police officers, the considerable laws enforced by the CFPB can be seen as cumbersome and restrictive. Financing police officers often argue that the CFPB's laws create unnecessary red tape, leading to even more documents and slower funding processing. Guidelines like the TILA-RESPA Integrated Disclosure (TRID) policy and the Ability-to-Repay (ATR) demands, while targeted at protecting customers, can lead to hold-ups in closing bargains and raised functional costs.

{kind=link}

Latest Posts

Nelson Nash Infinite Banking

Is Bank On Yourself Legitimate

Becoming Your Own Banker And Farming Without The Bank